Home Improvements That Affect Homeowners Insurance Coverage

When homeowners plan improvements, they usually think about boosting comfort, increasing home value, or modernizing outdated spaces. But one area that often gets overlooked is homeowners insurance. Certain upgrades can lower your premiums, while others may raise them—and in some cases, failing to notify your insurer can even leave you underinsured.

Understanding how home improvements affect your coverage is essential, especially in today’s market where replacement costs and risk factors are continually shifting. Here’s a breakdown of the most common upgrades that impact homeowners insurance and what every homeowner should keep in mind.

1. Adding a Pool or Spa

A backyard pool or spa can make your home feel like a private resort, but it also increases liability risk. Insurance impact:

Your liability coverage may need to be increased.

You may be required to install safety features like fencing or self-latching gates.

Premiums usually go up due to higher risk.

Tip: Before breaking ground, confirm what your insurer requires to stay fully covered.

2. Kitchen and Bathroom Remodels

These upgrades add significant value and often increase the cost to rebuild your home. Insurance impact:

Higher replacement value means your dwelling coverage might need an adjustment.

Premiums may increase slightly due to increased rebuild costs.

Tip: Keep receipts and detailed records of your renovation costs.

3. Roofing Upgrades

A new roof isn’t just a great selling point—it’s also one of the best improvements for insurance savings. Insurance impact:

Premiums often decrease, especially if you install impact-resistant or fire-resistant materials.

Some insurers offer credits for certain roof styles or materials.

Tip: Ask your contractor for documentation on materials and wind/fire ratings.

4. Electrical, Plumbing, or HVAC Updates

Older systems pose fire and water-damage risks. Updating them can dramatically improve safety. Insurance impact:

Premiums may decrease due to reduced risk.

Insurers may require updates in older homes to maintain coverage.

Tip: Save proof of system upgrades—this can result in insurance discounts.

5. Building an Addition or ADU

An addition increases the size and replacement cost of your home. ADUs (Accessory Dwelling Units) also introduce new liability factors, especially if rented out. Insurance impact:

You will likely need more dwelling coverage.

Rental uses may require additional liability or landlord coverage.

Tip: Always notify your insurer before renting out the space.

6. Installing Smart Home Security Systems

Security upgrades are a win for both safety and insurance savings. Insurance impact:

Premiums often decrease when you install monitored alarm systems, smart cameras, water leak detectors, or fire alarms.

Many insurers offer tiered discounts based on the level of monitoring.

Tip: Provide your insurer with proof of active monitoring.

7. Upgrading Windows or Adding Storm Shutters

Particularly in areas prone to windstorms or wildfires, more resilient windows reduce risk. Insurance impact:

Potential premium discounts.

Some insurers require certain window strengths in high-risk zones.

Tip: Ask your insurer if the upgrade qualifies for hazard-mitigation credits.

8. Landscaping and Tree Removal

Believe it or not, your yard can influence your insurance. Insurance impact:

Removing dead or hazardous trees can lower risk of damage during storms.

Adding features like retaining walls or extensive hardscaping may raise replacement costs.

Tip: Document tree removal or defensible-space improvements for wildfire-prone areas.

Why It’s Important to Notify Your Insurance Company

Any major home improvement that increases value, risk, or structural components can affect whether you have adequate coverage. If you fail to update your policy:

You may be underinsured in a total-loss event.

Claims can be denied for unreported features (e.g., a pool or rental unit).

You could miss out on discounts that save you money.

A quick call to your insurance agent before and after improvements ensures your coverage stays accurate and your investment is protected.

Final Thoughts

Home improvements are an exciting way to build equity and enhance comfort—but they also reshape your insurance profile. Whether you’re adding safety features or expanding your living space, staying proactive with your insurer helps avoid surprises and ensures your home is fully protected.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

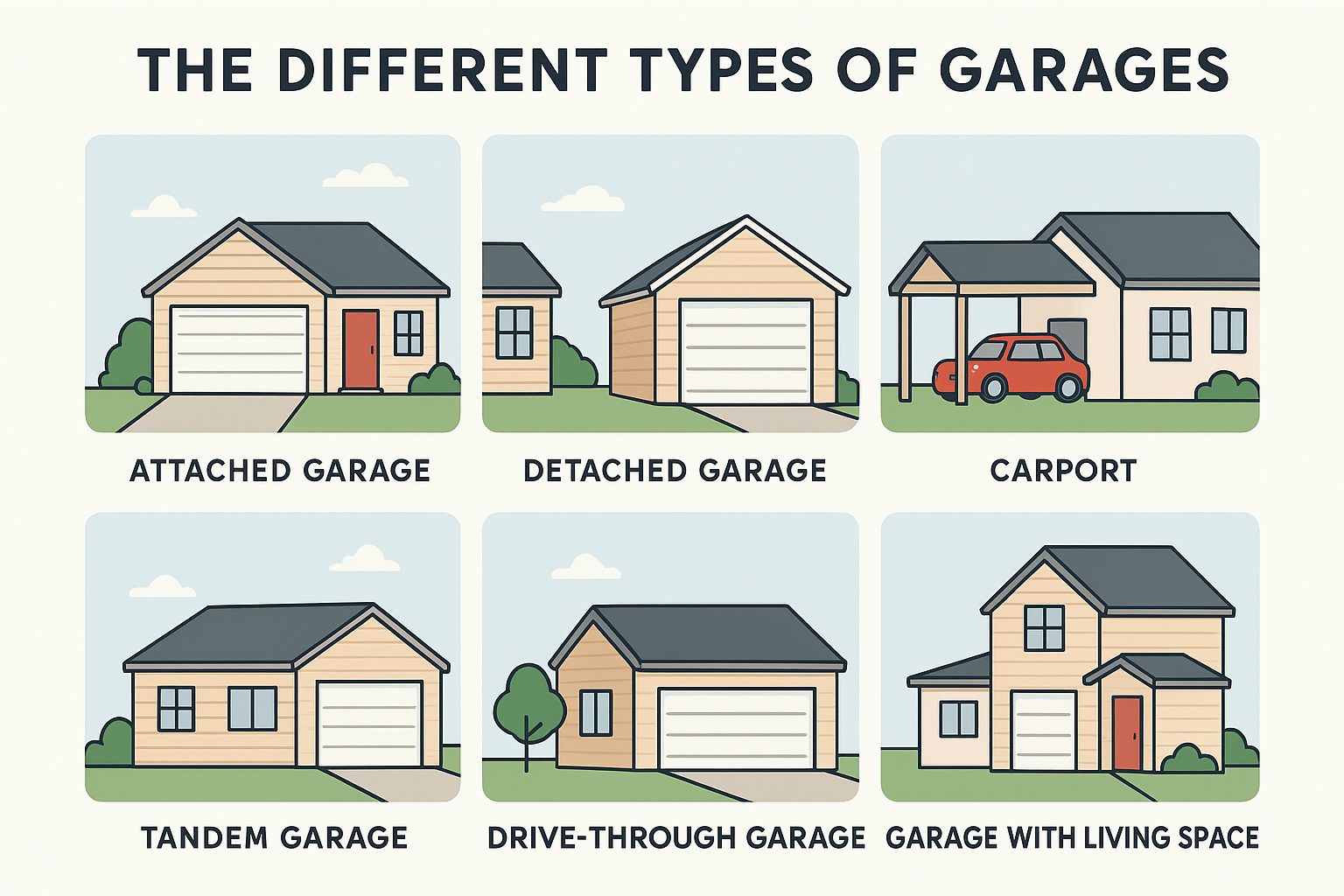

🏠 The Different Types of Garages: Which One Fits Your Home Best?

When buying or selling a home, the garage might not be the first thing you think about — but it’s often a key feature that adds both convenience and value. Garages come in many styles and configurations, each offering unique benefits depending on your needs, lot size, and budget. Here’s a breakdown of the most common types of garages you’ll encounter in real estate.

1. Attached Garage

An attached garage is built directly into the home and shares one or more walls with the main structure. This is the most common style in suburban neighborhoods.

Pros:

Convenient access to the home, especially in bad weather.

Easier to heat or cool since it’s part of the main structure.

Typically more affordable to build than a detached garage.

Cons:

May transmit noise or fumes into the house.

Can limit expansion options or home design flexibility.

Best for: Homeowners who value convenience and accessibility.

2. Detached Garage

A detached garage stands separate from the home, often connected by a walkway or breezeway.

Pros:

Greater design flexibility and curb appeal.

Ideal for workshops, hobby spaces, or home gyms.

Less noise and fumes in the living space.

Cons:

Less convenient in bad weather.

Typically more expensive to build due to additional foundation and utilities.

Best for: Buyers who want a separate workspace or prioritize aesthetics.

3. Carport

A carport is a covered parking area with open sides, offering protection from the sun and rain without the cost of a full enclosure.

Pros:

Budget-friendly and quick to build.

Provides basic protection for vehicles.

Can be added to homes with limited space or strict zoning.

Cons:

Offers limited security and protection.

May not add as much resale value as a full garage.

Best for: Homeowners in mild climates or those looking for an affordable parking solution.

4. Tandem Garage

A tandem garage is designed to fit two or more vehicles end-to-end rather than side-by-side.

Pros:

Efficient use of narrow lots.

Provides extra storage or workspace.

Cons:

Inconvenient for daily use — the first car must be moved to access the second.

Not ideal for multiple drivers with conflicting schedules.

Best for: Narrow lots or homeowners who use one vehicle regularly and the other for storage or seasonal use.

5. Drive-Through Garage

A drive-through garage has doors on both ends, allowing vehicles to enter and exit from different sides — great for properties with dual street access.

Pros:

Excellent for boat or trailer storage.

Easy maneuverability — no backing out required!

Cons:

Requires more land and additional doors (higher cost).

Best for: Homes on large lots or those with rear street or alley access.

6. Garage with Living Space (Accessory Dwelling Unit or Bonus Room)

Some garages include a living space above or beside — often a guest suite, home office, or ADU (Accessory Dwelling Unit).

Pros:

Adds living space and rental potential.

Can significantly increase property value.

Cons:

More expensive to build and maintain.

May require special permits or zoning approval.

Best for: Homeowners looking to maximize property utility or generate income.

Final Thoughts

The right type of garage depends on your lifestyle, property layout, and long-term goals. Whether it’s a simple carport or a fully equipped garage with a loft, this feature can greatly influence your home’s functionality — and its appeal to buyers.

If you’re considering adding or remodeling a garage, consult with your local real estate professional and check city zoning regulations to ensure your investment adds value where it counts most.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

How Much Does a Pool or Spa Add to Your Home’s Value?

For many homeowners in San Diego County, a backyard pool or spa isn’t just a luxury — it’s a lifestyle upgrade. But if you’re thinking about buying, selling, or refinancing, you might wonder: how much does a pool or spa actually add to a home’s value according to appraisers?

1. Pools and Spas Are Lifestyle Features, Not Always Cash in the Bank

While pools and spas are visually appealing and can make your home feel like a private resort, appraisers view them differently than structural features like kitchens or bathrooms. Pools are generally considered amenities, meaning they can enhance the appeal of a home but may not always provide a dollar-for-dollar return on investment.

2. Regional Differences Matter

In hotter climates like Southern California, pools are more desirable than in cooler areas. An appraiser in San Diego County recognizes that a well-maintained pool or spa can make a home more competitive in the market. However, the value added often depends on neighborhood norms. If most homes in your area have pools, it might add less value because it’s expected.

3. Typical Appraiser Adjustments

Appraisers typically make adjustments for pools and spas in the following ways:

Quality & Condition: A professionally installed, well-maintained pool adds more value than a DIY or poorly maintained one.

Size & Features: Standard pools add some value, but features like waterfalls, heating, or spa integration can increase adjustments.

Market Preference: If buyers in the area actively seek homes with pools, the appraiser may assign a higher value.

Maintenance & Safety: Older pools that require repairs or pose safety hazards might even result in a negative adjustment.

On average, appraisers often adjust for pools or spas in the range of $20,000–$50,000, depending on the factors above — though this can vary widely based on location and comparable sales.

4. Buyer Considerations

Not all buyers see pools as a benefit. Some may view them as high-maintenance features that increase water bills, chemical upkeep, and liability risks. This can influence how much an appraiser considers the pool in the final valuation.

5. Maximizing Pool Value

To make your pool a positive factor in your home’s appraisal:

While pools and spas rarely recoup 100% of their installation costs, they can boost your home’s marketability and help your property stand out — especially in San Diego’s competitive market. For sellers, a clean, updated, and well-maintained pool often translates to higher buyer interest, faster sales, and potential appraisal adjustments.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

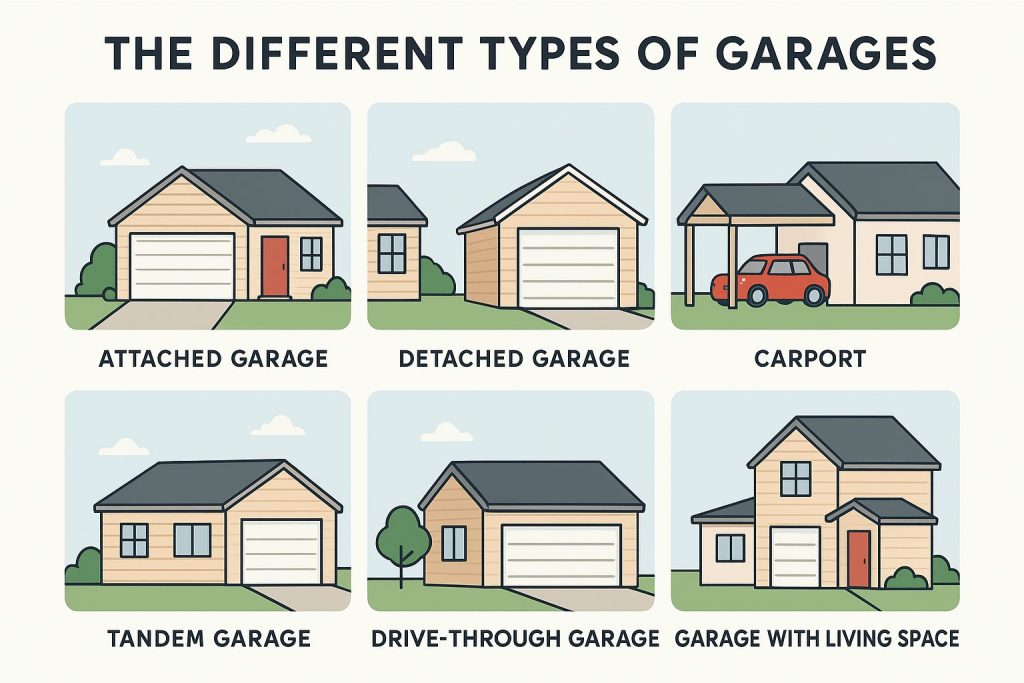

How Trees Affect Property Values: A Real Estate Perspective

Trees do more than make a property look attractive — they can directly influence home value, marketability, and buyer perception. Depending on their type, location, and condition, trees can either boost a home’s value or create concerns that impact pricing and demand. Here’s how trees factor into real estate value.

How Trees Can Increase Property Value

1. Curb Appeal Mature, healthy trees add character and visual appeal. Homes with attractive landscaping often sell faster and can command higher prices because first impressions matter.

2. Shade and Energy Efficiency Strategically placed trees can reduce cooling costs by providing natural shade. In warmer climates, buyers often see this as a long-term cost-saving benefit.

3. Privacy and Noise Reduction Trees act as natural buffers from neighbors and streets, creating a sense of privacy that many buyers are willing to pay for.

4. Environmental and Lifestyle Appeal Trees improve air quality, support wildlife, and create inviting outdoor spaces — features increasingly valued by eco-conscious buyers.

5. Higher Appraised Value Well-maintained landscaping, including trees, can contribute to higher appraisals when it enhances overall property appeal and usability.

When Trees Can Hurt Property Value

6. Maintenance and Cost Concerns Large or aging trees require pruning, watering, and occasional removal. Buyers may factor these future expenses into their offers.

7. Risk to Structures Trees planted too close to the home can threaten foundations, roofs, plumbing lines, and sidewalks through invasive root systems.

8. Insurance and Liability Issues Dead or damaged trees may increase insurance premiums or raise liability concerns if branches pose a risk to neighboring properties.

9. Overgrown or Unmanaged Landscaping Neglected trees can make a property feel dark, crowded, or poorly maintained, turning buyers off rather than impressing them.

10. View Obstruction In areas where views are a major selling point, trees that block ocean, mountain, or city views can significantly reduce value.

What Buyers and Sellers Should Know

Healthy, well-placed trees generally add value

Poorly maintained or hazardous trees can lower offers

Location and species matter as much as size

Professional trimming before listing can improve marketability

Bottom Line

Trees are a powerful but often overlooked factor in real estate value. When properly maintained and thoughtfully positioned, they can enhance beauty, comfort, and resale value. When neglected or poorly placed, they can create costly challenges. For homeowners considering selling, a tree assessment may be just as important as staging or paint.

If you’re unsure whether your trees are helping or hurting your home’s value, a local real estate professional can provide guidance tailored to your market.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

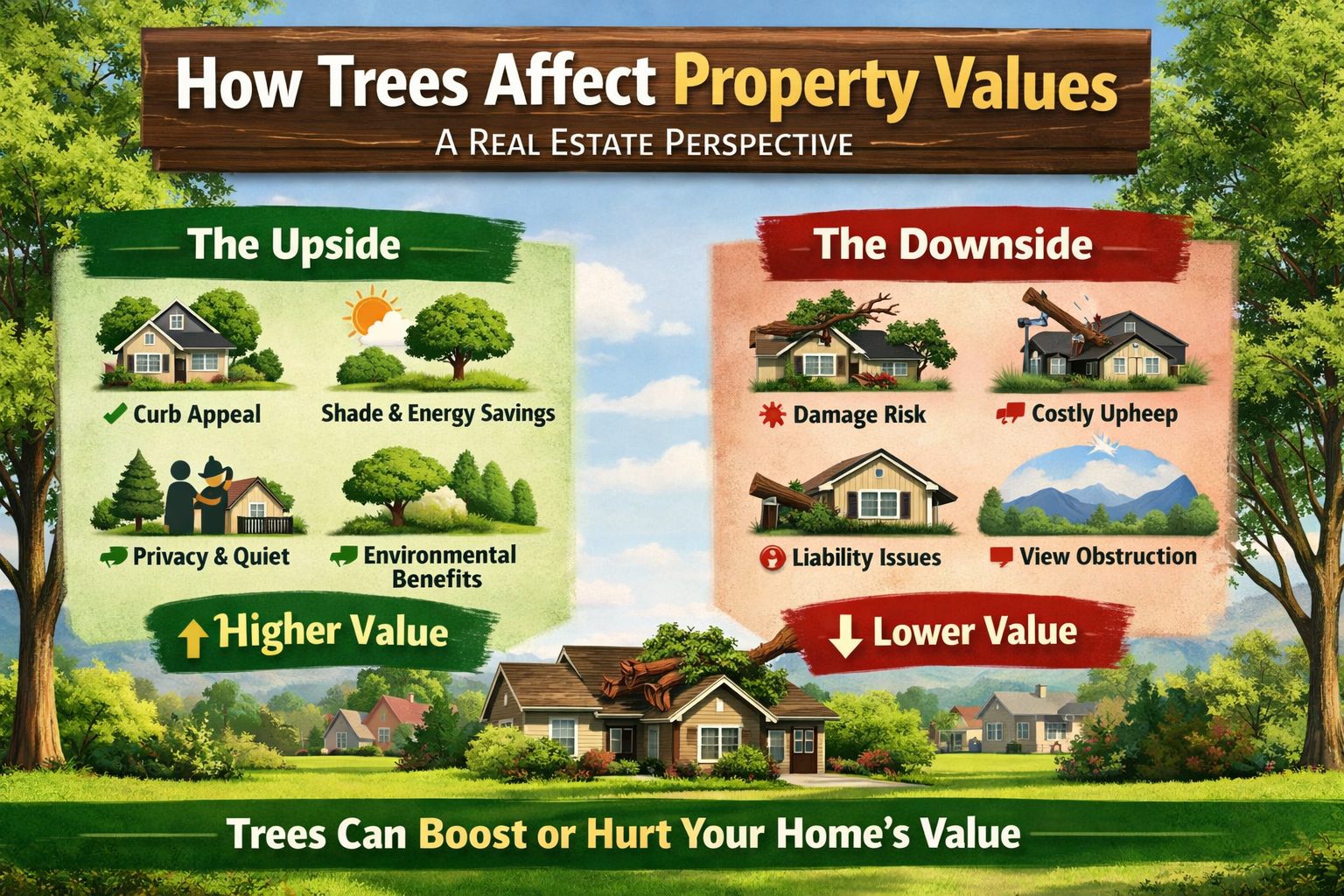

The Tax Benefits of Owning a Home in San Diego County

Buying a home in San Diego County doesn’t just provide stability, a place to call your own and the chance to build equity—it also opens up a number of tax benefits you should know about. Of course, every homeowner’s situation is different so you’ll want to consult your tax professional. But here’s a broad, blog-style overview of the key tax advantages (and some of the limitations) of home ownership in California (and thus for San Diego County).

1. Mortgage Interest Deduction

One of the classic tax benefits of home-ownership is the ability to deduct the interest on your mortgage.

If you itemize your deductions on your federal tax return, you may deduct the interest you pay on a qualified home loan for your primary residence (and in many cases a second home).

Under current rules: For mortgages taken out after December 15, 2017, the deduction limit is on interest paid on up to $750,000 of mortgage debt for married couples filing jointly (or $375,000 if married filing separately). For mortgages taken out before that date, older rules (e.g., $1 million limit) may apply.

If you moved money around (for example a home-equity loan or line of credit), note: interest you pay may only be deductible if the borrowed funds were used to “buy, build or substantially improve” the home.

What this means for a San Diego homeowner:

If you buy a home, the interest component of your mortgage in early years is often relatively high (because amortization). Deducting this can reduce your taxable income, lowering your tax bill.

But a caveat:

You must itemize your deductions in order to claim mortgage interest. If your total itemized deductions are less than the standard deduction (see later), then the benefit may be minimal or non‐existent.

2. Property Tax Deduction & SALT Cap

Another major benefit: property taxes you pay are in many cases tax‐deductible. But there are also important limits to understand.

Property Tax Deduction

Homeowners in California can deduct property taxes (and certain other local taxes) on their federal returns, when they itemize.

In California, for example, there’s also a “homeowners’ exemption” that lowers the assessed value of your principal residence by $7,000 (which modestly reduces the property tax owed).

SALT (State and Local Tax) Deduction Cap

Under federal tax law (the Tax Cuts and Jobs Act of 2017 and subsequently), the deduction for state and local taxes (SALT) — which includes property tax, state income tax, and local sales tax — is capped at $10,000 (for married filing jointly) for tax years 2018 through 2025.

Accordingly: Even if you pay $12,000 (or $15,000) in property taxes in San Diego County, your deduction for federal purposes may be limited by that $10,000 cap (if your state income tax + property tax + sales tax combined exceed it).

What this means for a San Diego homeowner:

Since San Diego is a higher-cost area, property tax bills can be sizeable. The ability to deduct them is real, but the SALT cap often limits how much benefit you get at the federal level. At the state level (California), there is no SALT cap effect, so you may still deduct full property tax on your state tax return (depending on your circumstances) because California does not impose that same $10k cap for its own tax calculus.

3. Capital Gains Exclusion When You Sell

Owning your home gives you a powerful benefit when it’s time to sell: the capital gains tax exclusion.

Under federal law, if you’ve lived in your home as your primary residence for at least two of the last five years, you can exclude up to $250,000 of capital gain from your income if you are single, or up to $500,000 if married filing jointly.

This means: Suppose you buy a home in San Diego County, live in it for 2+ of the last 5 years, and sell it for a higher price—if your gain falls under those thresholds, you may owe no federal capital gains tax on that portion.

In California, your gain may still be subject to the state tax, but the federal exclusion is considerable.

Why this matters in San Diego:

With home prices and appreciation in many San Diego neighborhoods, the potential gain can be large. The exclusion gives you peace of mind that a large portion (or all) of the gain may avoid federal tax—with proper planning.

In California, there are constitutional and statutory protections that benefit homeowners—not just tax deductions but structural advantages.

California Proposition 13 (1978) limits the property tax rate on real property to 1% of the assessed value (except for voter-approved local assessments) and restricts annual assessment increases of the taxable value of a property to a maximum of 2% per year, unless there is a change in ownership or new construction.

The “homeowners’ exemption” in California allows a reduction in assessed value of $7,000 for a qualified residence. (As noted above.)

Why this is beneficial:

Even though California property values (and thus taxes) may be high in San Diego County, these protections illustrate that tax burdens don’t rise uncontrollably. Your tax is limited to 1% of assessed value (plus voter‐approved amounts), and the assessed value only increases modestly each year (so long as you don’t sell or significantly alter the property). That stability is a meaningful advantage of home-ownership in California.

5. Energy-Efficient Improvement Credits & Home Office Deductions

Beyond the big ticket items, there are additional tax wins for homeowners who make certain investments.

If you install renewable energy systems (solar panels, battery storage) or make qualified energy-efficient home improvements, you may be eligible for federal tax credits (for example, the Residential Clean Energy Credit) or state incentives.

If you run a business from home (for example you’re self-employed or work remotely and qualify), you may be able to claim a home office deduction (in certain cases) which allocates a portion of mortgage interest, utilities, repairs and depreciation to that business area.

Relevance for San Diego homeowners:

Given California’s push toward renewable energy and San Diego’s generally favorable climate for solar, this is a meaningful added benefit. If you’re doing business from home or using part of the home exclusively and regularly for business, those deductions may apply.

6. Putting It All Together: What A Homeowner in San Diego Should Know

Here are some practical considerations and pitfalls.

✅ Advantages

You get to deduct mortgage interest (if you itemize) — that can be one of the largest deductions in early years.

You can deduct property taxes at the federal level (within limits) and fully (typically) at the California state level.

You benefit from the capital gains exclusion when you sell your primary residence (assuming you meet conditions).

California’s Proposition 13 and the homeowners’ exemption give structural tax stability and protection.

Additional credits or deductions for energy improvements or certain home uses may further benefit you.

⚠️ Limitations / Things to Watch

To get most of these benefits, you must itemize your deductions. If your itemized deductions (mortgage interest + property tax + other deductible expenses) don’t exceed the standard deduction, it may not “pay” for its complexity. For example: Some homeowners discover they still take the standard deduction because it’s larger.

The SALT deduction cap (state and local taxes limitation) means that in high tax states like California, the benefit of property tax deduction is limited on the federal side: you can deduct only up to $10,000 (for the combined state income + property + sales taxes) for many taxpayers.

The mortgage interest deduction limit ($750k) means if you purchase a very expensive home with a large loan, a portion of the interest might not be deductible under the newer rules.

Deductions change year to year—as do tax laws—so staying updated is critical.

💡 Tips for San Diego Homeowners

Keep accurate records: mortgage interest statements (Form 1098), property tax bills, receipts for any home improvements, and documentation if you use a home office.

Early in home-ownership, run projections: How much interest will I pay in year 1? How high are my property taxes (San Diego County has higher home values, and thus higher taxes). Will I exceed the standard deduction when adding everything up?

Consider state vs federal implications: On the California return, you may have different deduction rules than federally.

When you sell or refinance, consult tax advice: Because of the capital gains exclusion and potential recapture or reassessment triggers in California, planning ahead helps.

For energy upgrades: If you’re in San Diego and installing e.g. solar panels, you may reduce your utility bills and claim credits — a double win.

Conclusion

Owning a home in San Diego County brings more than just the emotional and lifestyle benefits—it offers tangible tax advantages, including interest deductions, property tax deductions (within limits), capital‐gain exclusions, structural tax protections via Proposition 13, and potential credits/deductions for energy improvements or business use.

That being said: Buying a home primarily for tax savings isn’t usually wise. The tax benefits help, but they typically don’t overwhelm the costs of home-ownership (maintenance, insurance, property tax, mortgage rates, etc.). Instead think of them as one of several factors in the overall decision.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

What Makes a Community Walkable? A Homebuyer’s Guide

When buyers talk about wanting a “walkable neighborhood,” they’re often envisioning more than just sidewalks and streetlights. Walkability is about convenience, lifestyle, health, and community connection—all rolled into one. Whether you’re shopping for a home in North San Diego County or simply curious about what truly defines a walkable community, here are the key features to look for.

1. Convenient Access to Everyday Essentials

A walkable community places your daily needs within a short stroll.

This includes:

Grocery stores

Coffee shops

Restaurants

Pharmacies

Local services (dry cleaning, barber, fitness studios)

The idea is simple: fewer car trips, more fresh air.

2. Safe and Connected Infrastructure

Walkability starts with thoughtful design. Look for:

Wide, well-maintained sidewalks

Pedestrian-friendly street crossings

Traffic-calming features like speed bumps and roundabouts

Adequate lighting for evening walks

These elements create a safe, comfortable path for residents of all ages.

3. Proximity to Parks and Recreation

Whether it’s a quiet neighborhood park, dog park, hiking trail, or a community center, recreational spaces encourage people to walk more often. In San Diego County, this often means access to coastal trails, canyon routes, and large public parks that make walking not just practical, but enjoyable.

4. A Mix of Housing and Land Use

Walkable communities often offer a blend of:

Single-family homes

Townhomes

Condos

Mixed-use buildings

When shops, residences, and businesses are woven together, the neighborhood becomes more vibrant and accessible.

5. Public Transportation Options

Even if you prefer walking, it helps to live near reliable transit. A walkable area typically provides easy access to:

Bus stops

Rapid transit lines

Trolley stations (in areas like downtown, La Mesa, and UTC)

This connectivity reduces dependence on cars and adds flexibility to your daily routine.

6. Inviting Streetscapes and Community Spaces

Walkability isn’t only about distance—it’s also about enjoyment. The best walkable communities include:

Shade trees

Benches and seating areas

Public art

Clean, welcoming storefronts

These features encourage people to linger, socialize, and explore.

7. A Strong Sense of Community

Walkable areas naturally bring neighbors together. When people see each other regularly—at the local café, market, or on evening walks—it strengthens community ties and enhances quality of life.

Why Walkability Matters in Real Estate

Homes in walkable neighborhoods often enjoy:

Higher property values

Better long-term demand

Lower transportation costs

Healthier lifestyles

For buyers in San Diego County, a walkable community can be a major advantage—especially as traffic concerns and gas costs continue to rise.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

🏡 The Home Buying Timeline: How Long Does It Really Take to Purchase a House?

Buying a home is one of the biggest financial decisions you’ll make—and one of the most common questions is: “How long does the process actually take?” The answer depends on your preparation, the market, and financing—but here’s a clear, realistic timeline to guide your expectations.

🔍 Step 1: Preparation & Pre-Approval (1–2 Weeks)

Before you even start house hunting, you’ll want to get your finances in order.

What happens here:

Review credit, income, and debt

Meet with a lender

Get pre-approved for a mortgage

Why it matters:

Pre-approval strengthens your offer and helps you understand your true budget—critical in competitive markets like San Diego County.

🏠 Step 2: Home Search (2–8 Weeks or More)

This is often the most unpredictable part of the process.

What affects timing:

Inventory levels

Your price range

How specific your needs are

Market competition

Pro tip:

In a fast-moving market, buyers may find a home in days. In slower markets, it could take months.

✍️ Step 3: Making an Offer & Negotiation (3–7 Days)

Once you find the right home, things move quickly.

This stage includes:

Submitting an offer

Negotiating price and terms

Seller acceptance

In competitive situations, decisions can happen within hours.

🔎 Step 4: Escrow & Due Diligence (21–30 Days)

This is the most structured phase of the transaction.

Key milestones:

Home inspection (within first 7–10 days)

Appraisal ordered by lender

Loan underwriting

Contingency removals

This period ensures the home and financing meet all requirements before closing.

🔑 Step 5: Closing (3–5 Days)

You’re almost there!

Final steps:

Signing loan documents

Final walkthrough

Recording the sale

Getting the keys

⏱️ Total Timeline: 30–90 Days (Typical)

Fast scenario: ~30 days (cash buyer or quick decision-making)

Average: 45–60 days

Longer timeline: 90+ days (extended home search or financing delays)

📍 What Can Speed Things Up?

Full loan pre-approval (not just pre-qualification)

Flexible home criteria

Working with an experienced local agent

Strong, clean offers

⚠️ What Can Slow Things Down?

Low inventory

Financing complications

Appraisal issues

Extensive negotiations or repairs

🏁 Final Thoughts

While the home buying process can feel complex, understanding the timeline helps you stay confident and in control. Whether you’re buying your first home or your next investment, preparation and the right team can make all the difference.

If you’re considering buying in North San Diego County, knowing these timelines can help you plan strategically and compete effectively in today’s market.

Thinking about making a move? Now is the time to start the conversation and map out your personalized home buying timeline. Start searching for free!

Steve Cardinalli

Real Estate Professional, 01323509 (760) 814-0248 Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

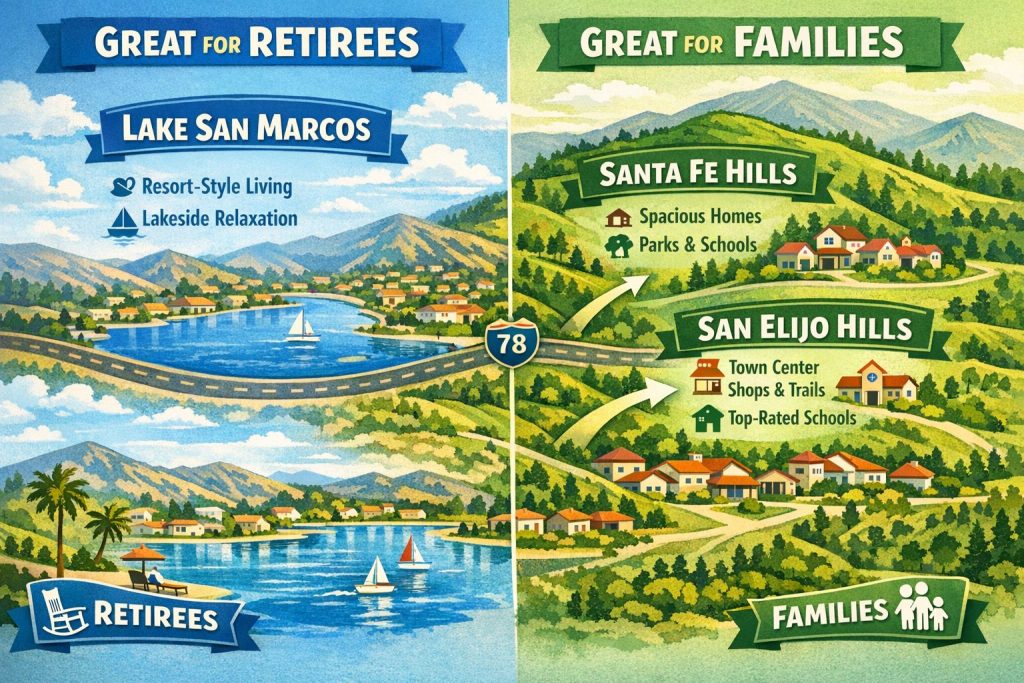

Lake San Marcos vs Santa Fe Hills vs San Elijo Hills

1. Lake San Marcos

Location & Community:

Nestled around a private, scenic lake in San Marcos, offering a small-town, resort-like feel.

Popular with retirees and those seeking a slower pace of life; active 55+ communities are prevalent.

Lifestyle & Amenities:

Walking trails around the lake, fishing, boating, and a golf course.

Many social clubs, community centers, and senior-focused activities.

Quiet and serene, less traffic and fewer crowds.

Housing:

Mix of single-family homes, condos, and villas.

Homes often have lake or golf course views.

Generally higher age-restricted communities with moderate to higher price points.

Pros:

Scenic and tranquil, resort-style amenities.

Tight-knit, slower-paced community.

Cons:

Less ideal for young families; fewer schools nearby.

Some areas may feel isolated from shopping and urban conveniences.

2. Santa Fe Hills

Location & Community:

Part of North San Marcos, newer master-planned neighborhoods.

Designed for families and professionals; suburban feel.

Lifestyle & Amenities:

Modern parks, trails, and green belts.

Community events geared towards families and children.

Good access to shopping and freeway connections.

Housing:

Larger, modern single-family homes.

Higher elevation means some homes have valley or hillside views.

Price points tend to be higher due to newer construction and lot sizes.

Pros:

Family-friendly, safe, and modern.

Quick access to amenities and schools.

Cons:

Less “resort” feel; more suburban and structured.

Can feel less scenic compared to Lake San Marcos.

3. San Elijo Hills

Location & Community:

Located in the coastal hills of San Marcos; highly planned community.

Designed for families, but has a mix of ages and lifestyles.

Lifestyle & Amenities:

Town-center concept with shops, restaurants, and cafes.

Walking trails, parks, and community events (farmers’ markets, concerts).

Schools are highly rated; strong focus on family life.

Housing:

Mix of single-family homes and some townhomes.

Homes are often architecturally appealing, with some hillside views.

Price point is comparable to Santa Fe Hills but can vary based on lot and view.

Pros:

Walkable town-center lifestyle.

Family-oriented, strong school district.

Beautiful, maintained landscaping and hillside views.

Cons:

Slightly higher density than Santa Fe Hills or Lake San Marcos.

Less privacy in some neighborhoods.

Summary Table

Feature

Lake San Marcos

Santa Fe Hills

San Elijo Hills

Best For

Retirees, quiet lifestyle

Families, professionals

Families, active lifestyle

Housing Type

Condos, villas, single-family

Modern single-family

Single-family, some townhomes

Community Feel

Resort-like, relaxed

Suburban, safe

Walkable, family-friendly

Amenities

Lake, golf, walking trails, social clubs

Parks, trails, modern amenities

Parks, trails, town center, shops

School Access

Limited

Good

Excellent

View / Scenery

Lake & golf views

Hills & valley views

Hillside views, landscaped

Price Range

Moderate-high

High

High

Key Takeaways:

Lake San Marcos is ideal for tranquility and scenic, lake-focused living—more for retirees than young families.

Santa Fe Hills is modern and family-focused, with larger homes and good suburban amenities.

San Elijo Hills blends family living with a walkable town-center feel and strong schools, plus some scenic hillside views.

Are you thinking of moving to San marcos, CA? Contact me, Steve Cardinalli, for a list of homes in your budget or start your search here: San Marcos, CA.

Steve Cardinalli

Real Estate Professional, 01323509 (760) 814-0248 Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

Do I Have to Disclose If My Home Is in a Flood Zone When Selling It?

When selling a home, transparency isn’t just good practice—it’s the law. One of the most common questions sellers ask is whether they’re required to disclose if their property is located in a flood zone. The short answer? Yes. In California (and most states), sellers must disclose this information to potential buyers as part of the natural hazard disclosure process.

Understanding Flood Zone Disclosures

A flood zone is an area that has a certain level of risk for flooding as determined by the Federal Emergency Management Agency (FEMA). Flood maps categorize areas based on their likelihood of flooding—ranging from minimal risk to high-risk floodplains that require mandatory flood insurance for federally backed mortgages.

If your property lies within one of these zones, that information must be shared with buyers before closing.

In California, state law (Civil Code §1103) requires sellers to provide buyers with a Natural Hazard Disclosure (NHD) Report. This document, typically prepared by a third-party company, informs buyers if the property is located in any of six state-mapped hazard zones, including:

A Special Flood Hazard Area (FEMA flood zone)

A Very High Fire Hazard Severity Zone

A Wildland Fire Area

An Earthquake Fault Zone

A Seismic Hazard Zone (liquefaction or landslide risk)

A State Responsibility Area for wildfires

Failing to provide this disclosure can expose sellers to legal liability, including potential lawsuits for nondisclosure.

Why Flood Zone Disclosures Matter

Disclosing a flood zone isn’t just about following the law—it’s about protecting both buyer and seller.

For buyers: It allows them to plan for flood insurance and understand potential risks.

For sellers: It demonstrates honesty and reduces the risk of future disputes or claims of misrepresentation.

Buyers are far more likely to trust a seller who is transparent from the beginning.

What If You’re Unsure?

If you’re not sure whether your property is in a flood zone, your real estate agent or NHD provider can help obtain a reliable report. You can also check FEMA’s Flood Map Service Center online for a free map of your property’s risk area.

Bottom Line

Yes, you must disclose if your home is in a flood zone when selling it in California. Providing a complete Natural Hazard Disclosure report ensures compliance with the law and helps build trust with your buyers. It’s a small step that can prevent big problems down the road.

Be the first to know about the market trend in your community at Neighborhood News

🏡 San Diego County Real Estate Market Insights — March 2026

📈 Spring Market Gaining Traction — But Still Competitive

The San Diego housing market continues its slow, steady evolution as we settle into the spring buying season. Local data and recent market signals show:

Investor demand remains significant in major California markets, including San Diego, as investors expand activity even amid affordability challenges.

Mortgage rates nationally have dipped slightly, with the 30‑year average recently at ~6.33%.

This rate environment — while higher than the ultra‑low pandemic years — is encouraging some sidelined buyers back into the market.

For San Diego specifically, buyer interest is rebounding after winter, but affordability and inventory levels still shape the pace of activity.

📊 Local Inventory & Price Dynamics

San Diego’s housing inventory and pricing reflect a nuanced marketplace:

Inventory remains below balanced levels, showing more options than in recent peaks but still under the traditional “six‑month supply” that indicates equilibrium.

Some neighborhoods may see increased for‑sale activity, especially as sellers target peak viewing weeks in spring. Historically, listings mid‑April tend to sell faster and often for more.

Luxury home inventory growth has pushed the market time for high‑end properties (above $2 M) upward, meaning slower sales in that segment compared with lower‑priced tiers.

💡 What this means for your clients: The market isn’t “stuck,” but pricing and timing are key — especially for sellers in higher price brackets and buyers trying to balance cost with value.

🔍 Buyer Trends You’re Seeing Locally

Many San Diego buyers and agents are reflecting a few key realities in 2026:

📍 Affordability Challenges Still Loom

Even though mortgage costs softened slightly in recent months, buyers in San Diego still struggle with high home prices relative to local wages — with median prices above $1 M in many parts of the county.

📍 More Properties Are Staying on Market Longer

With increased listings compared to a year ago, homes that aren’t competitively priced are staying on the market longer, particularly outside the most desirable price points and neighborhoods.

📍 Buyers Are More Disciplined

Agents report that today’s buyers are:

More cautious about overbidding

Focused on properties priced correctly

Monitoring total ownership costs — including taxes, HOA fees, and insurance, not just mortgage payments

These behaviors reflect broader national trends around hidden housing costs rising faster than wages, squeezing affordability.

📈 What This Means for Sellers

Here’s how you might position your listings right now:

Price with precision: Overpricing can lengthen days on market and push buyers toward other options.

Capitalize on spring demand: Traditionally, mid‑April through May attracts more buyers and faster sales.

Highlight value: Features like remodeled kitchens, outdoor living spaces, and energy‑efficient upgrades resonate with buyers balancing costs and lifestyle.

📉 What This Means for Buyers

For buyers in San Diego County:

Don’t wait for huge price drops: Local data hasn’t shown any major price collapses — only modest shifts and neighborhood variability.

Get financing ready today: Even small declines in mortgage rates can improve affordability.

Think long game: Buying in strong markets like San Diego often rewards patience and strategic negotiation.

📣 Final Takeaways

San Diego County’s housing market in March 2026 is balanced between opportunity and challenge:

✔ Inventory is slowly increasing but still modest compared to long‑term norms.

✔ Mortgage rates are stabilizing near 6%, giving some buyers confidence to act.

✔ Buyers are disciplined, and sellers must price strategically to capture attention.

✔ Hidden ownership costs — taxes, insurance, HOA — are climbing nationwide and matter locally too.

Bottom line: Contact me, Steve Cardinalli, if you’re listing a property this spring, timing and pricing precision will be your edge. And for buyers, readiness and realistic budgeting are key to securing a home in this still‑competitive San Diego market.

Steve Cardinalli

Real Estate Professional, 01323509 (760) 814-0248 Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link