Buying a home starts long before you fall in love with a listing — it starts with knowing your numbers. Taking time now to check in on your finances can make the buying process smoother and far less stressful down the road. When you understand where you stand, you can move forward with confidence and clarity. 🏡 If homeownership is on your radar, let’s talk through what this looks like for you. My inbox is open!

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

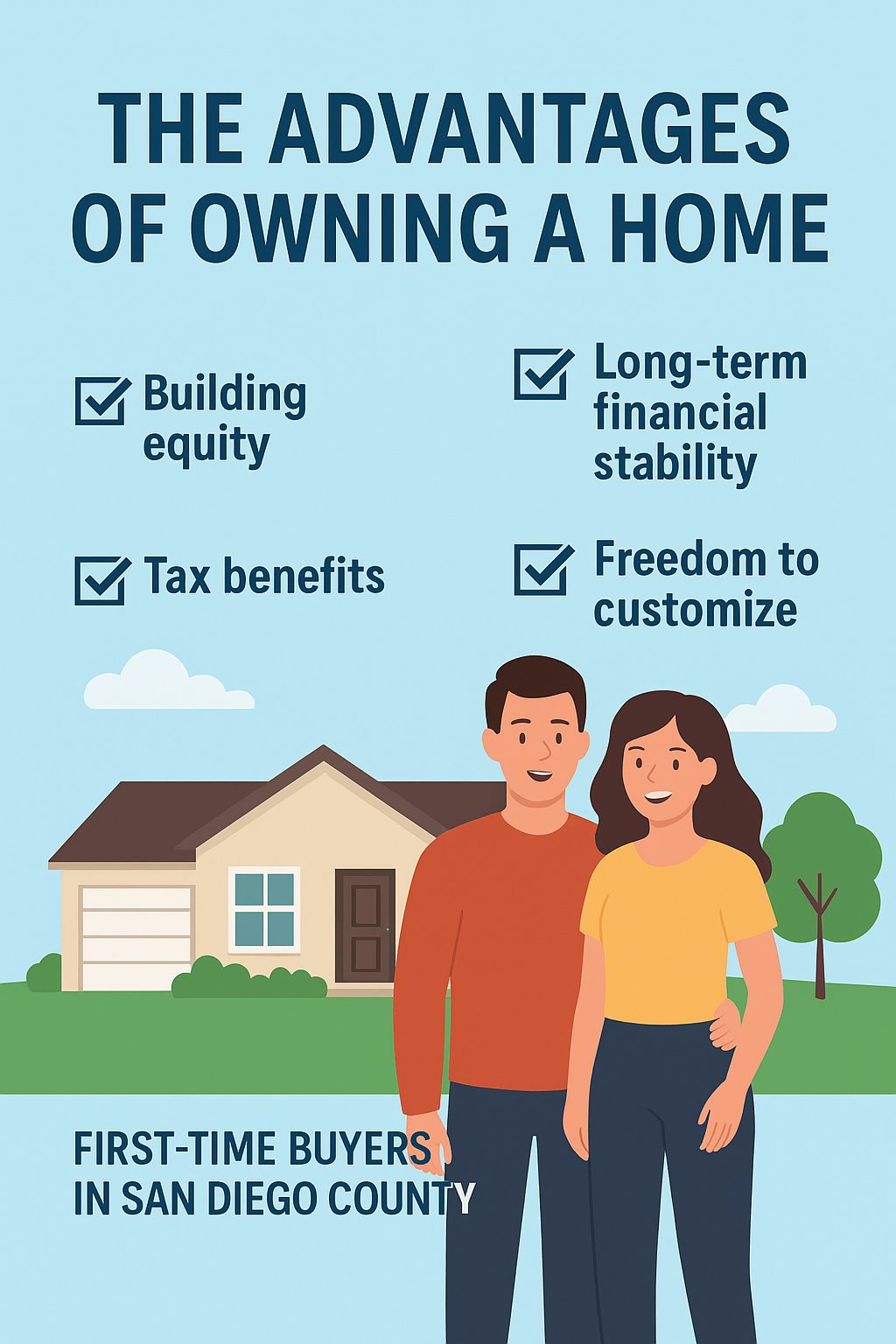

Owning a home is one of the most rewarding achievements in life — and one of the smartest financial decisions you can make. Beyond the pride of having a place to truly call your own, homeownership offers a range of benefits that can enhance your financial stability, personal freedom, and long-term wealth.

1. Building Equity Over Time

Every mortgage payment you make helps you build equity — the portion of the home you actually own. Unlike rent, which offers no return, your payments increase your stake in a valuable asset that typically appreciates over time. This equity can later be used for home improvements, debt consolidation, or other investments.

2. Long-Term Financial Stability

When you own your home, you gain protection from rising rents and unpredictable housing costs. A fixed-rate mortgage keeps your monthly payments stable, helping you plan your finances with confidence. Over time, your housing costs may even decrease relative to your income, giving you more financial breathing room.

3. Tax Benefits

Homeownership can offer several tax advantages. Mortgage interest and property tax payments may be deductible, which can help lower your taxable income. These benefits can make owning a home more affordable compared to renting over the long term.

4. Freedom to Customize

As a homeowner, you have the freedom to make your house truly your own. Want to remodel the kitchen, paint the walls, or add a backyard patio? You can personalize your space to match your lifestyle and taste without asking a landlord for permission.

5. A Sense of Stability and Belonging

Owning a home provides a sense of permanence and connection to your community. You can establish roots, build relationships with neighbors, and contribute to local schools and businesses — all while enjoying the comfort of a place that’s yours.

6. Potential for Appreciation

Over time, most real estate increases in value. While markets can fluctuate, homeowners who hold onto their properties typically see appreciation that contributes to their overall net worth. Real estate has long been a cornerstone of wealth building in America.

7. A Legacy for Your Family

Your home is more than just an investment — it’s a legacy. It can be passed down to future generations, providing financial security and a place filled with family memories for years to come.

Final Thoughts

Owning a home offers stability, financial growth, and the opportunity to create a space that truly reflects who you are. If you’ve been considering buying a home, now is a great time to explore your options and see how ownership could benefit your future.

Owning a home isn’t just about where you live — it’s about building the life you want.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

How PODS Can Help You Sell Your Home Faster—and Move Smarter

Preparing a home for sale isn’t just about pricing and marketing—it’s also about presentation. One of the biggest challenges sellers face is clutter. That’s where PODS® offers a smart, flexible solution that can make a real difference.

Declutter to Stage, Stage to Sell

PODS provides portable storage containers that are delivered right to your driveway. This allows sellers to pack away excess furniture, personal items, and seasonal belongings before the home hits the market. With less clutter, rooms appear larger, cleaner, and more inviting—helping buyers focus on the home itself rather than what’s inside it.

A well-staged, clutter-free home often photographs better, shows better, and can even sell faster and for more money.

A Seamless Transition After the Sale

One of the biggest advantages of PODS is flexibility. After your home sells, the same container can be used for your move—whether you’re relocating locally or out of the area. No rushed packing, no multiple moves, and no unnecessary stress.

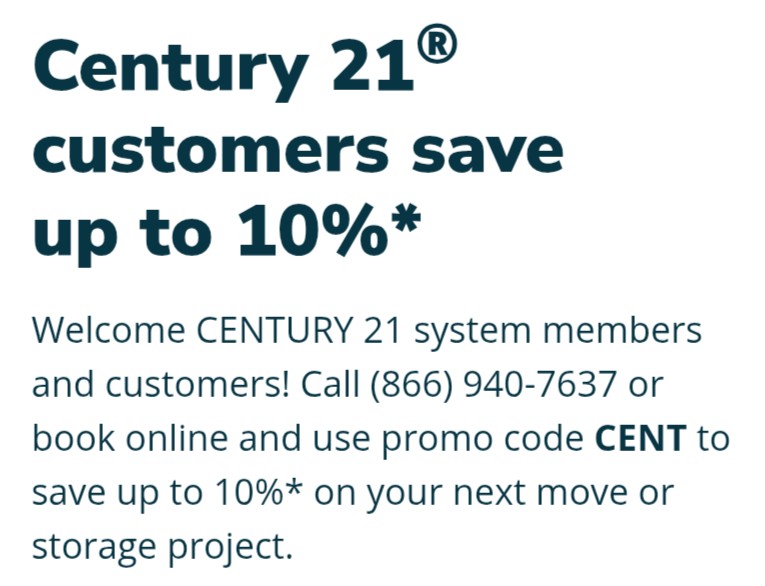

Exclusive Savings for Buyers and Sellers

As an added bonus, clients can save up to 10% on their next moving and storage project when using PODS with a special partner promotion.

How to redeem:

Visit: pods.com/century21

Call: 866-940-7637

Use Promo Code: CENT

A Smarter Way to Move

From pre-listing decluttering to post-sale moving, PODS offers a convenient, efficient solution that supports a smoother real estate transaction from start to finish.

If you’re thinking about selling—or planning your next move—this is a tool worth considering.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

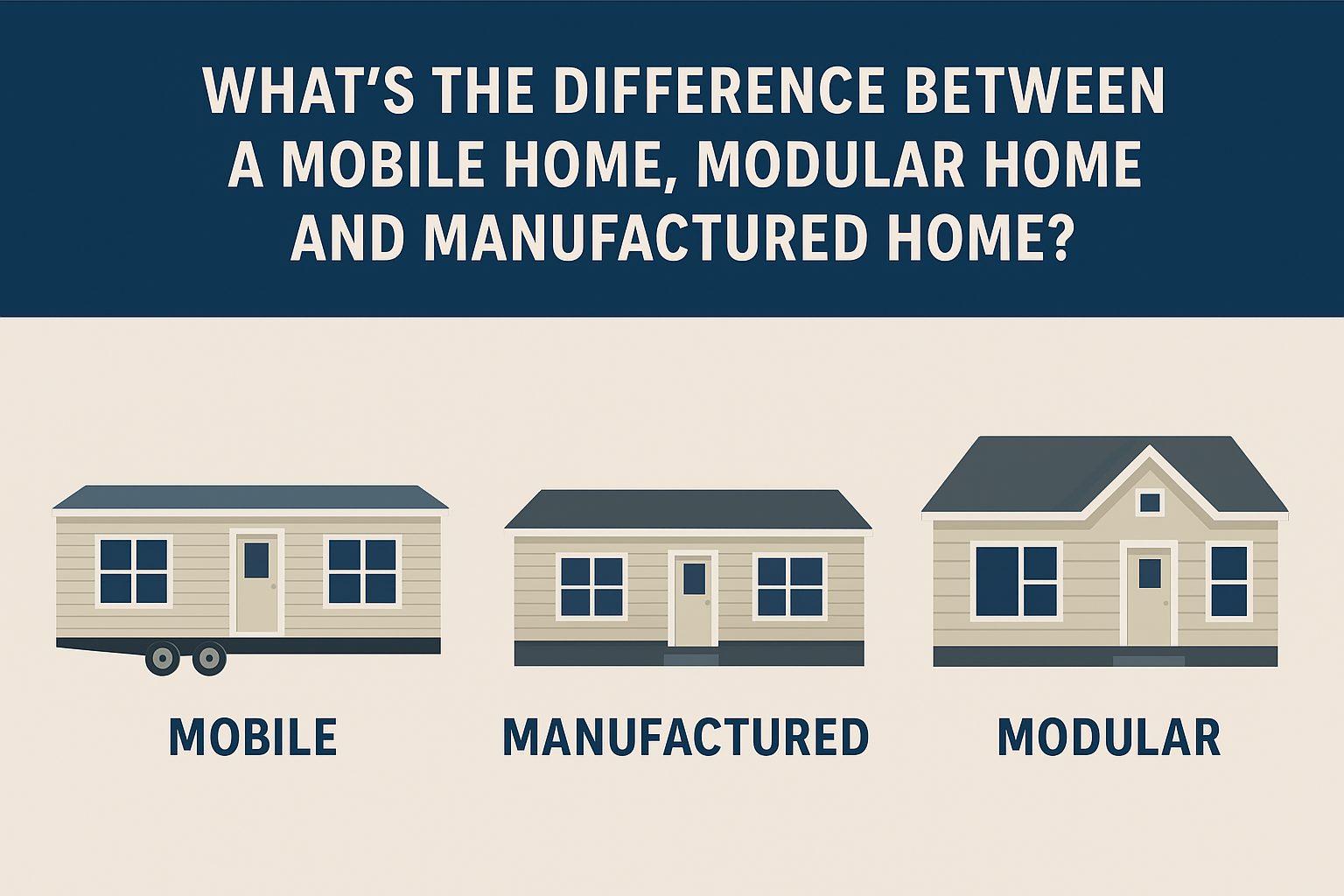

🏠 What’s the Difference Between a Mobile Home, Modular Home, and Manufactured Home?

When searching for affordable housing in San Diego County, you may come across terms like mobile home, manufactured home, and modular home. These housing types can look similar—but there are important differences in how they’re built, regulated, and financed. Understanding these distinctions can help you make a more informed decision when buying or selling.

🚐 Mobile Homes (Built Before 1976)

Definition:

A mobile home refers to a factory-built home constructed before June 15, 1976—the date when federal construction standards took effect under the HUD Code (Housing and Urban Development).

Key Points:

Built before national safety and construction standards were established.

Typically built on a steel chassis and transported to a site, often in a mobile home park.

Can be moved, though doing so is costly and may not meet local zoning rules.

Financing can be more difficult; some lenders classify them as personal property (not real estate).

In short: All mobile homes are factory-built—but not all factory-built homes are mobile homes.

🏡 Manufactured Homes (Built After 1976)

Definition:

A manufactured home is the modern version of a mobile home, built after June 15, 1976, under strict federal HUD Code regulations. These homes must meet national standards for construction, energy efficiency, fire safety, and structural integrity.

Key Points:

Built entirely in a factory, then transported to the property site.

Placed on a permanent or semi-permanent foundation.

Each section carries a HUD certification label (red tag) verifying compliance with national standards.

Eligible for financing similar to traditional homes if on owned land with a permanent foundation.

Available in single-wide, double-wide, or triple-wide layouts.

In short: Manufactured homes are the updated, safer, and better-built successors to mobile homes.

🧱 Modular Homes

Definition:

A modular home is also factory-built, but it follows local and state building codes, not federal HUD standards. It’s built in sections (modules) in a factory and assembled on-site, much like traditional homes.

Key Points:

Must meet the same local building codes as site-built homes.

Typically placed on a permanent foundation.

Can look identical to traditional stick-built homes once completed.

Usually appreciate in value similar to site-built homes.

Financing options are the same as for conventional homes.

In short: Modular homes are “real houses” built in a factory and assembled on-site—combining efficiency with traditional quality.

⚖️ Quick Comparison Chart

Feature

Mobile Home

Manufactured Home

Modular Home

Built Before/After 1976

Before

After

Ongoing

Building Code

None (pre-HUD)

Federal HUD Code

Local/State Codes

Foundation

Chassis or semi-permanent

Permanent or semi-permanent

Permanent

Financing

Limited (personal property)

Easier (real property eligible)

Traditional mortgage options

Appreciation

Usually depreciates

Varies

Often appreciates

Movable

Can be moved

Not intended to move

Not movable

🌴 Final Thoughts

Choosing between a mobile, manufactured, or modular home depends on your lifestyle, budget, and long-term goals. In San Diego County, manufactured and modular homes provide more stability, financing options, and resale potential—while mobile homes remain an affordable entry point for homeownership.

If you’re exploring these housing types or need help determining property value and financing options, I can help guide you through the process from start to finish.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

Why Now Is a Good Time for Home Buyers as Interest Rates Ease

After a challenging period of elevated mortgage rates, the real estate market is beginning to shift in favor of home buyers. Recent declines in interest rates are improving affordability and creating new opportunities for buyers who may have been waiting on the sidelines. Here’s why today’s rate environment makes now a smart time to buy.

1. Lower Interest Rates Increase Buying Power

Even small drops in interest rates can have a significant impact on monthly payments. As rates ease, buyers can qualify for higher-priced homes while keeping payments manageable—or enjoy lower payments on the same home. This increased purchasing power expands options and improves overall affordability.

2. Reduced Monthly Payments Improve Long-Term Value

Lower rates don’t just help at closing—they affect the total cost of ownership over time. A reduced interest rate can save buyers tens or even hundreds of thousands of dollars over the life of a loan, making today’s environment especially attractive for long-term homeowners.

3. Buyers Can Act Before Competition Returns

As interest rates fall, more buyers re-enter the market. Those who act early often benefit from less competition, better selection, and stronger negotiating power. Waiting until rates drop further may mean facing multiple-offer situations and rising prices again.

4. Sellers Are Still Offering Incentives

While rates are improving, many sellers are still motivated and open to concessions. Buyers may be able to secure closing cost credits, price adjustments, or even temporary rate buy-downs—stacking these benefits on top of already-lower interest rates.

5. Refinancing Is Still an Option

Buying while rates are trending downward provides flexibility. If rates continue to fall, refinancing remains an option. But locking in a purchase now allows buyers to secure a home before prices adjust upward in response to increased demand.

6. Market Stability Supports Smarter Decisions

With rates stabilizing and affordability improving, buyers can make informed decisions without the urgency seen in overheated markets. This creates a healthier buying experience and reduces the risk of overpaying.

7. Homeownership Locks in Predictable Housing Costs

While rents may continue to fluctuate, a fixed-rate mortgage offers long-term payment stability. Securing a lower interest rate today can help protect buyers from future housing cost increases while building equity over time.

Bottom Line

Lower interest rates are reopening the door for buyers. Combined with motivated sellers and improving inventory, today’s market offers a strategic opportunity for those ready to act before competition and prices respond to falling rates.

If you’re considering buying, understanding how today’s rates affect your purchasing power can make all the difference.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

How the Recent Interest Rate Reduction Impacts Buyers and Sellers

After a long stretch of elevated mortgage rates, the recent reduction in interest rates is beginning to reshape the real estate landscape. While rates are still higher than the historic lows of a few years ago, even a modest drop can have meaningful effects on both buyers and sellers. Here’s how the shift is playing out across the market.

What Lower Rates Mean for Buyers

1. Improved Affordability

A lower interest rate directly reduces a buyer’s monthly mortgage payment. Even a small rate decrease can translate into hundreds of dollars saved each month, increasing overall purchasing power.

2. Expanded Buying Options

With improved affordability, buyers may qualify for higher-priced homes or feel more comfortable choosing properties that previously stretched their budgets. This can reopen neighborhoods or home styles that were recently out of reach.

3. Renewed Buyer Confidence

Many buyers paused their plans during periods of rate volatility. Rate reductions often bring buyers back off the sidelines, increasing showing activity and loan applications.

4. Competitive Pressure Returns

As more buyers re-enter the market, competition can increase—especially for well-priced, move-in-ready homes. Buyers may need to act more decisively and be prepared with strong offers.

What Lower Rates Mean for Sellers

1. Larger Buyer Pool

Lower rates expand the number of qualified buyers, which can lead to increased demand for listings—particularly in desirable price ranges.

2. Stronger Offers

With buyers saving on financing costs, sellers may see cleaner offers with fewer concessions, stronger down payments, or shorter contingencies.

3. Improved Market Momentum

Rate reductions often boost market activity overall, reducing days on market and improving seller confidence.

4. Pricing Discipline Still Matters

While demand may increase, today’s buyers remain price-conscious. Homes that are overpriced or poorly presented may still sit, even in a lower-rate environment.

The “Lock-In” Effect Begins to Ease

One major challenge over the past two years has been the so-called “lock-in effect,” where homeowners with ultra-low mortgage rates were reluctant to sell. As rates come down, some of that hesitation begins to fade, potentially leading to more inventory and better balance between supply and demand.

What This Means for the Market Overall

More transactions as buyers and sellers find common ground

Moderate price stability, rather than dramatic spikes or drops

Increased negotiation, especially as inventory gradually improves

This rate reduction doesn’t signal a return to the frenzied markets of the past, but it does point toward a healthier, more active real estate environment.

Bottom Line

Lower interest rates are a positive development for both buyers and sellers—but strategy still matters. Buyers should focus on long-term affordability, not just monthly payments, while sellers should price and present their homes thoughtfully to capture renewed demand.

Whether you’re considering buying, selling, or just watching the market, understanding how rate changes affect real estate can help you make smarter, more confident decisions.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

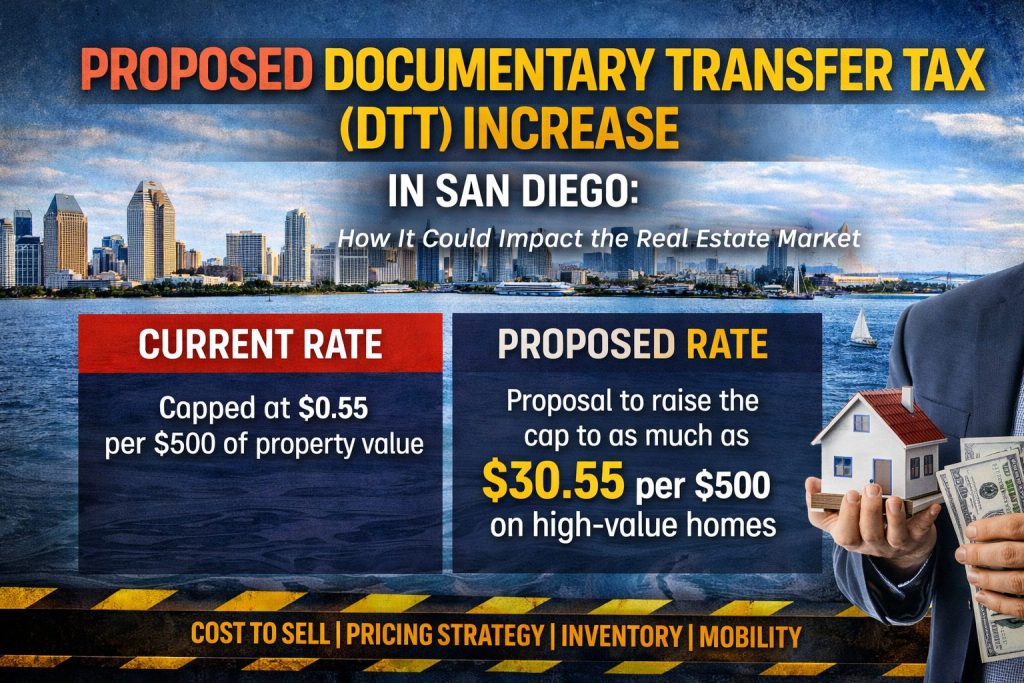

Proposed Documentary Transfer Tax (DTT) Increase in San Diego: What It Could Mean for the Real Estate Market

San Diego is considering a significant change to the Documentary Transfer Tax (DTT)—a fee paid when real property changes ownership. While still a proposal, the potential increase has generated strong opinions across the real estate community due to its possible impact on sellers, buyers, investors, and overall market activity.

Understanding how the DTT works—and how the proposed increase differs from the current structure—is critical for anyone considering a real estate transaction in San Diego.

What Is the Documentary Transfer Tax?

The Documentary Transfer Tax is a one-time tax assessed at the transfer of property ownership, typically calculated based on the sales price. In most San Diego transactions, the tax is customarily paid by the seller, although it can be negotiated in the purchase agreement.

DTT revenue is generally allocated to local government services, which may include infrastructure, housing programs, or general fund expenses.

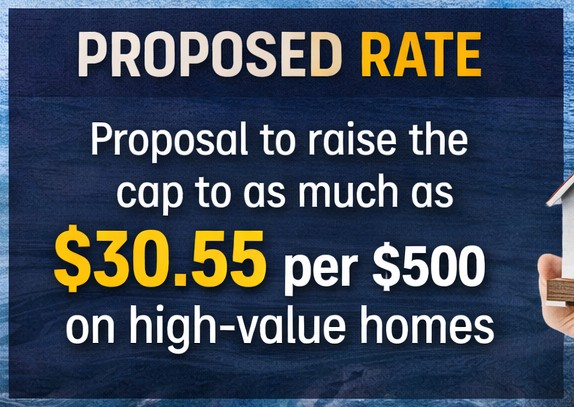

Current Rate vs. Proposed Increase

Under the existing framework:

Current Rate: The DTT is capped at $0.55 per $500 of property value.

Under the proposal being discussed:

Proposed Rate: The cap could increase to as much as $30.55 per $500 of property value on high-value homes.

If approved, this would represent a substantial increase in transaction costs for qualifying properties, applied only at the time of sale, not annually like property taxes.

Potential Impact on Sellers

Higher Cost to Sell

A higher DTT directly increases seller closing costs. On higher-priced homes, the proposed rate could result in significantly higher taxes due at closing, potentially reaching tens of thousands of dollars.

Changed Selling Strategies

Sellers may respond by:

Increasing listing prices to offset the tax

Becoming less flexible during negotiations

Delaying sales until market or policy conditions change

This could contribute to reduced housing inventory, particularly in higher price brackets.

Potential Impact on Buyers

Although buyers don’t typically pay the DTT directly, the cost rarely disappears:

Sellers may price homes higher

Fewer listings could increase competition

Negotiations may become tighter

Over time, this can place upward pressure on prices, especially in desirable neighborhoods.

Effects on Investors and Luxury Properties

High-value homes and investment properties are expected to be the most affected.

Reduced profit margins for investors

Fewer flips and speculative transactions

Potential redirection of capital to nearby markets with lower transaction costs

This could slow transaction volume in certain segments without necessarily improving affordability.

Housing Affordability: Help or Hindrance?

Supporters argue that increased DTT revenue could fund affordable housing initiatives. Critics point out that higher transaction costs are often passed along, potentially increasing prices or limiting mobility.

In real estate, added costs are rarely absorbed without consequence—they usually shift elsewhere in the market.

Broader Market Implications

If implemented, a higher DTT could lead to:

Fewer overall transactions

Longer homeowner hold periods

Reduced market mobility

Short-term slowdowns in higher price tiers

While markets tend to adjust over time, policy changes like this can create near-term friction.

The Real Estate Takeaway

The proposed increase to San Diego’s Documentary Transfer Tax underscores how local policy decisions can directly affect real estate behavior. Whether you’re planning to buy, sell, or invest, understanding how transaction costs factor into timing and pricing decisions is more important than ever.

As the proposal continues to evolve, details such as price thresholds, exemptions, and implementation timelines will be critical.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

How a Ban on Wall Street Investment in Single-Family Homes Could Impact Real Estate

In recent years, large institutional investors—often referred to as “Wall Street”—have become increasingly active in the single-family housing market. These investors typically purchase homes to operate as long-term rentals, particularly in high-growth metro areas. If a future policy were enacted to restrict or ban institutional investment in single-family homes, the real estate market could experience several notable shifts.

Below is an overview of the possible impacts on home prices, buyers, sellers, and renters, should such a policy take effect.

1. Increased Housing Supply for Owner-Occupants

One of the most immediate effects could be a rise in available inventory for traditional homebuyers. Institutional investors often compete directly with families by making all-cash, non-contingent offers. Removing or limiting this buyer pool could:

Reduce competition in certain price ranges

Increase the number of homes available to owner-occupants

Shorten bidding wars in entry-level and mid-priced neighborhoods

This could be especially impactful for first-time buyers who have struggled to compete in recent years.

2. Potential Softening of Home Prices in Some Markets

Investor-heavy markets could see modest price corrections. When demand from large-scale buyers is reduced:

Price growth may slow

Some neighborhoods could experience slight value declines

Appreciation may become more closely tied to local income growth rather than investor demand

However, this impact would likely vary widely by location. Markets with strong population growth and limited new construction may remain resilient.

3. Shifts in the Rental Market

Institutional investors play a significant role in supplying professionally managed single-family rentals. A reduction in this segment could lead to:

Fewer single-family rental options

Increased pressure on small, local landlords

Potential rent increases if rental supply tightens

In areas with high renter demand, this could create unintended affordability challenges for tenants.

4. Opportunities for Local Investors and Small Landlords

A ban targeting large institutional players may open the door for:

Individual investors

Small partnerships

Local real estate owners

These buyers may face less competition for properties, potentially revitalizing local ownership while keeping rental housing in the market.

5. Reduced Market Volatility

Institutional investors tend to scale buying and selling based on market conditions. Limiting their role could:

Reduce rapid swings in demand

Create a more stable, locally driven housing market

Tie home values more closely to fundamentals like employment and wages

This may appeal to long-term homeowners seeking steadier appreciation.

6. Regional Impacts Would Vary Significantly

Not all markets would be affected equally. Areas that could feel the biggest impact include:

Sun Belt cities with high investor activity

Suburban neighborhoods dominated by rental portfolios

Markets with large concentrations of build-to-rent developments

Conversely, markets with limited institutional ownership may see minimal change.

Final Thoughts

A ban on Wall Street investment in single-family homes could reshape parts of the housing market by easing competition for buyers, altering rental dynamics, and shifting ownership back toward individuals and local investors. While the goal of increasing housing affordability may benefit some buyers, the broader effects would depend heavily on local market conditions, housing supply, and renter demand.

As with any major policy change, the real estate market’s response would likely be uneven—creating both opportunities and challenges for buyers, sellers, investors, and renters alike.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

Who Could Own Land in the United States? A Brief History of Property Ownership

Land ownership has always been tied to power, wealth, and opportunity in the United States. But the right to own land hasn’t always been universal. Over the centuries, laws and social norms determined who could—and could not—own property, shaping today’s real estate landscape.

Here’s a timeline of how land ownership evolved throughout U.S. history.

Colonial America (1600s–1776): Land for the Few

In early America, land ownership was largely reserved for:

White European men

Wealthy settlers

Landowners approved by the Crown or colonial governments

Key limitations:

Women generally could not own land independently

Enslaved people were considered property, not owners

Indigenous tribes were displaced through treaties and force

Religious minorities sometimes faced restrictions

Land was power—and power was tightly controlled.

Post-Revolutionary Era (1776–1820s): Ownership Expands, Slowly

After independence, land ownership broadened, but not equally.

Who could own land:

White male citizens

Some immigrant men after naturalization

Widows in limited circumstances

Still excluded:

Women (unless widowed)

Native Americans

Enslaved Africans

Free Black Americans in many states

Property ownership often determined voting rights, reinforcing its importance.

Jacksonian Era & Westward Expansion (1820s–1860s): More Access, More Displacement

As the U.S. expanded west:

Property requirements for voting were dropped

Small landholdings became more common

Homesteading encouraged settlement

However:

Native Americans were forcibly removed from ancestral lands

Enslaved people remained barred from ownership

Free Black landowners faced legal and violent barriers

Women still lacked full property rights

Land was available—but not for everyone.

Post-Civil War & Reconstruction (1865–1900): Legal Rights vs. Reality

The Civil War ended slavery, and new amendments promised equality.

Legal changes:

Enslaved people were freed

Black Americans could legally own land

The Homestead Act allowed citizens to claim land

Practical barriers remained:

Discriminatory laws and practices

Sharecropping and debt systems

Violence and intimidation

Women’s property rights varied by state

Ownership was legal—but often unreachable.

Early 20th Century (1900–1940s): Segregation and Redlining

During this era:

Women increasingly gained property rights

Immigrants could own land after citizenship

But new obstacles emerged:

Racial covenants barred minorities from buying in many neighborhoods

Redlining denied loans to minority communities

Asian immigrants faced land ownership bans in some states

Government-backed policies reinforced inequality in housing.

Post-World War II (1945–1960s): Opportunity for Some

The housing boom transformed America.

Expanded access for:

White middle-class families

Veterans using VA loans

Still excluded or restricted:

Black Americans

Hispanic and Indigenous families

Women needing a male co-signer

Suburban growth created generational wealth—but unevenly.

Civil Rights Era (1960s–1980s): Equal Rights Under the Law

Major breakthroughs:

Fair Housing Act of 1968

Ban on discrimination based on race, color, religion, or national origin

Later protections for gender, disability, and family status

For the first time, land ownership was legally open to all Americans.

Modern Era (1990s–Today): Ownership with New Debates

Today:

Any U.S. citizen can own land

Non-citizens can generally own property

Women and minorities own property nationwide

Ongoing discussions include:

Foreign ownership of U.S. land

Corporate investors buying residential property

Affordability and access to housing

While laws now allow broad ownership, economic barriers still shape who buys land.

Why This History Matters in Real Estate Today

Understanding who could own land—and who couldn’t—helps explain:

Wealth gaps between generations

Neighborhood development patterns

Homeownership rates across communities

Why fair housing laws exist

Modern real estate isn’t just about location and price—it’s built on centuries of policy decisions.

Final Thoughts

Land ownership in the United States has evolved from a privilege reserved for a few to a right legally available to many. While progress has been made, history continues to influence today’s real estate market.

Knowing where we came from helps us better understand where the market—and property ownership—is headed.

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

As we welcome the New Year, it’s a perfect time to reflect on the past and look ahead to new opportunities—especially in real estate. A new year often brings renewed goals, fresh perspectives, and exciting possibilities for homeowners, buyers, and sellers alike.

For homeowners, the New Year is a chance to think about protecting and growing one of your most valuable assets. Whether that means planning strategic improvements, reviewing your home’s current value, or simply enjoying the comfort and stability your home provides, real estate continues to be a cornerstone of long-term wealth and security.

For buyers, a new year represents a clean slate. New inventory, changing market conditions, and evolving interest rates can create opportunities that didn’t exist just months ago. If homeownership is on your goal list this year, thoughtful planning and expert guidance can make all the difference.

For sellers, the New Year often sparks increased buyer motivation. Many people begin the year with serious plans to move, upgrade, or relocate. Preparing your home early—both in presentation and pricing—can position you strongly as the market gains momentum.

No matter where you are in your real estate journey, the New Year is about possibility, progress, and informed decisions. Here’s to a year filled with smart moves, new beginnings, and places you’re proud to call home.

Happy New Year, and cheers to a successful year ahead! 🥂

Steve Cardinalli

Real Estate Professional, 01323509

(760) 814-0248

Steve@Cardinalli.com www.Cardinalli.com

Century 21 Affiliated Fine Homes & Estates

Village Faire in Carlsbad Village

300 Carlsbad Village Dr, 223

Carlsbad, CA 92008

Be the first to know about the market trend in your community at Neighborhood News

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Preparing a home for sale isn’t just about pricing and marketing—it’s also about presentation. One of the biggest challenges sellers face is clutter. That’s where PODS® offers a smart, flexible solution that can make a real difference.

Preparing a home for sale isn’t just about pricing and marketing—it’s also about presentation. One of the biggest challenges sellers face is clutter. That’s where PODS® offers a smart, flexible solution that can make a real difference.